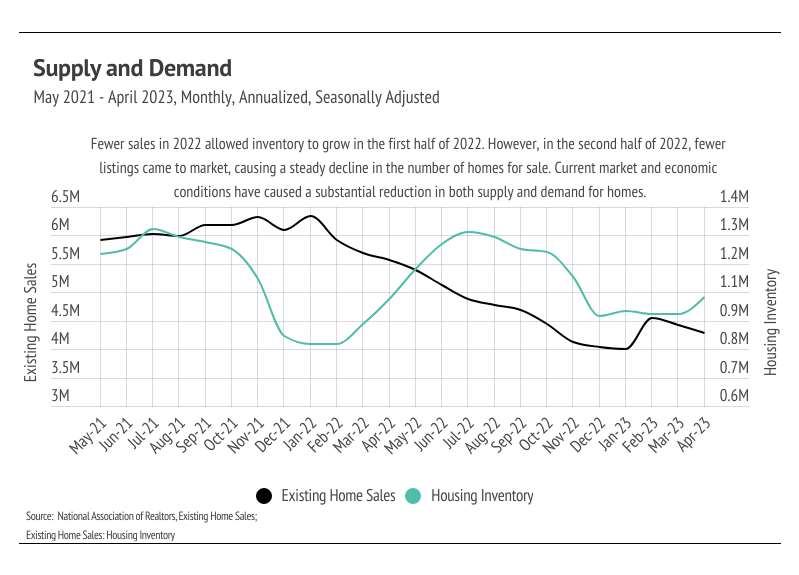

Happy Summer! Hard to believe it's pushing towards the end of June already. We are almost to the halfway point for the year! We are certainly seeing the first real, extended slow down we have seen in awhile. Properties are still selling, but for a little less in our market than they might have a year ago, and with not as many offers. There are always some that go quickly, even with multiple offers. But equally, we are seeing some beautiful homes, that show well and are priced right, sitting for some time before being sold. Interestingly, market activity overall has picked up a bit in June. This flies in the face of the last 4 or 5 years, especially post pandemic, when everyone got out of Dodge on June one and everything came to a screaming stop. But this year's market had a much slower start. Some of it may have been the unusual weather we had during the late winter with all the rain and storms, some due to the mortgage rates (more on this in a bit). In either case, what we have right now is a kind of balanced market. Sellers aren't quite getting the crazy overbids, but things are selling. Buyers, while the interests are higher, are also finding some negotiating room. I had the pleasure of helping a client purchase a home in Noe Valley last month. It was well priced and we kind of expected the usual feeding frenzy. Still, we took a shot at an offer under the asking price. And low and behold, we were the only ones who showed up and got it done! The sellers were still selling for more than they had paid for it 5 years ago, so in the end everyone came out doing well.

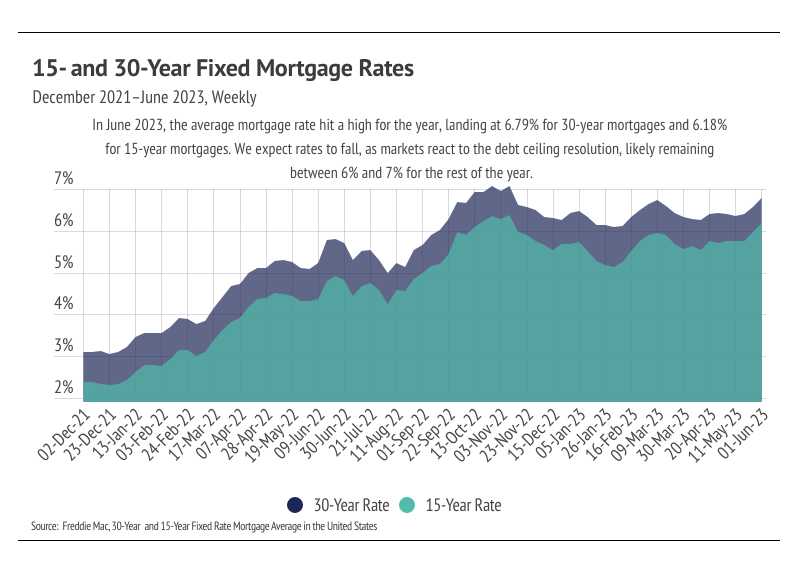

Interest Rates - I wanted to comment on this a little. Right now rates are hovering in the 6.25-7% range. For much of the last decade we got a bit spoiled with 2.5-4% rates. But historically speaking where we are now is still pretty good. My first home I bought in 2000 with an adjustable at 8.5% and thought myself lucky. Over the next few years rates dropped and I refinanced to lower payments. Eventually I sold and bought a new bigger place and my payments, because of the rate drops, remained roughly the same. The moral being that now is actually a great time to buy when prices are beginning to soften for the first time in a while. It's a smart move to buy at a lower price (with lower taxes) and a higher interest rate that can be refinanced in a few years, which will end up overall bringing your costs down. Check out the articles below for a more detailed look at the market trends.

On a personal note our family had the pleasure of graduating our first child from High School. To beat my parental chest just a little, Drake graduated from San Francisco's Ruth Asawa School of the Arts on the President's List with a perfect unweighted 4.0 GPA and got accepted into a half dozen great colleges. In the end he chose NYU's Tisch School where he will be a Theater Major (yup that apple didn't fall far). Monique and I are so proud and happy for Drake. Being a former New Yorker myself it is especially sweet. He'll be living and going to school in Greenwich Village just a few blocks from where I went to kindergarten.

ALSO - while I am bragging a little - I am really proud of our team here at Aethos. We were recognized again this year, for the 5th time in a row I might add, as being in the top 1.5% of Real Estate Professionals nationwide by Real Trends. And for that we thank all our wonderful clients and associates and friends with out whom it would not have been possible!

EXCLUSIVE AETHOS COMING SOON PROPERTIES

We have a few great homes coming in the next month or two:

West Portal/Forrest Hill - A lovely center patio home with almost 2000 square feet. Freshly renovated, this home will feature 3 bedrooms, 2 full baths including a brand new primary suite and bath that opens directly onto the level west facing rear yard. The home has a large living room with impressive fireplace and vaulted ceilings, a sizable formal dining room, breakfast room and remodeled kitchen. 2 car garage and extra storage. Price: TBD

Mountain View Townhouse - Located in one of the hottest markets in the Bay Area and also best school districts this 3 bedroom/2.5 bath home has just been extensively remodeled with new kitchen, bathrooms, flooring, lighting, paint and so much more. Part of a small complex that includes a lovely common pool (for someone else to maintain), the home is not attached to any other homes. It also feature several private and freshly landscaped patio spaces. Price: TBD

Bernal Heights Remodeled Home - This home has been more than taken down to the studs. It was rebuilt pretty much for the ground floor up including the creation of a massive 4 car, high ceilinged garage which was intended as well as a maker space for the owners. Above that the two levels of living space include 3 bedrooms and tewo new bathrooms. The first level includes a primary suite and bath with soaking tub and walk in closet, media/family room with unique skylight from the level above and a generous laundry room. The main floor features a large open living space with new kitchen with quartz counters and new high end appliances, dining area, office area and large living room with nano doors that open onto the intimate garden and hot tub. Two bedrooms and another new bath complete this level. There a views from both the front of the house West through the trees to Diamond Heights and also from the office and garden South over Bernal Hts and to the Bay. Price: TBD

Feel free to call me for more info on any of these amazing properties and estimated on market dates or for private showings. And please feel free to tell a friend.

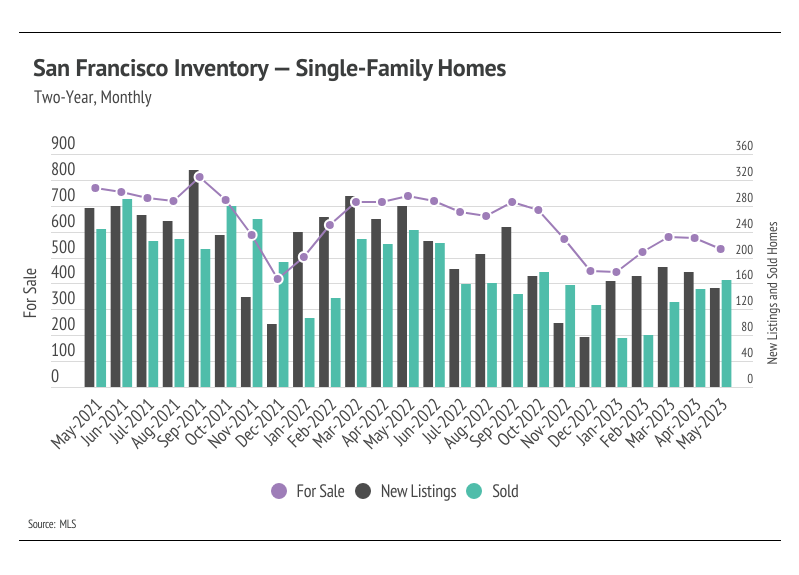

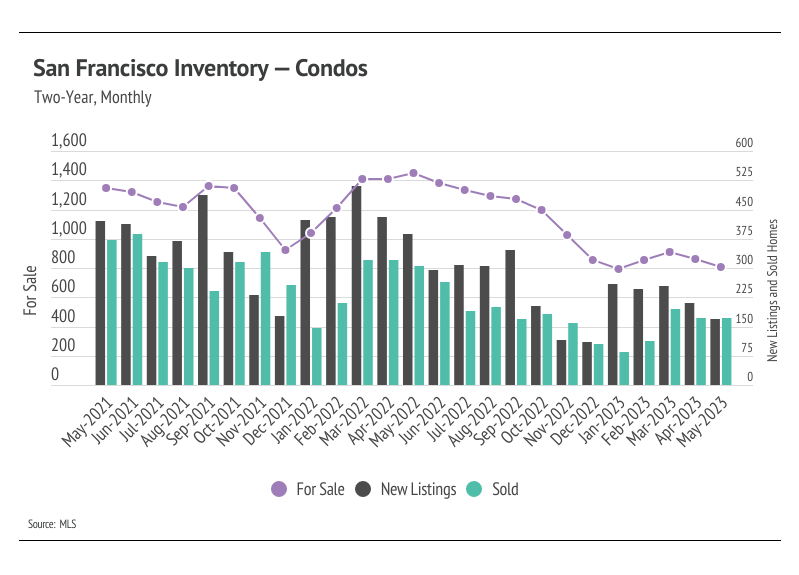

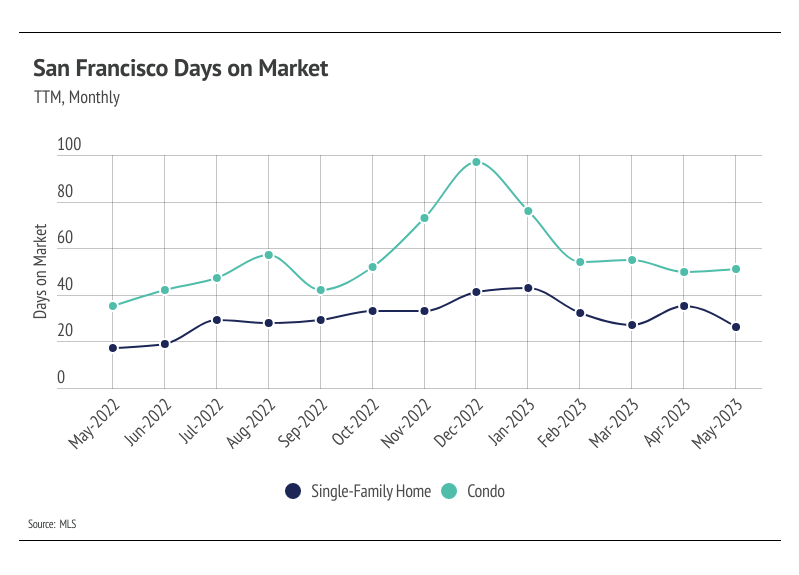

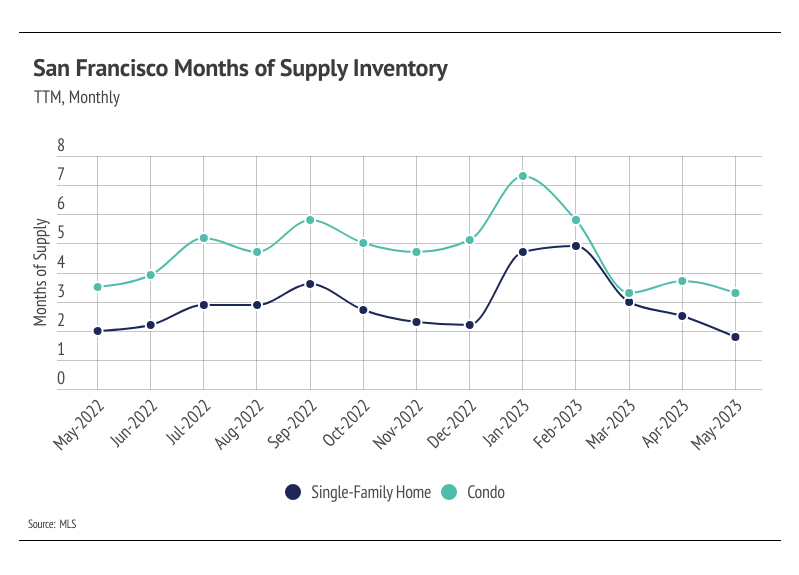

Please remember we are your local real estate experts, and we feel it’s our duty to give you, our valued client and friends, all the information you need to better understand our local real estate market. Whether you’re buying or selling, we want to make sure you have the best, most pertinent information, so we’ve put together this monthly analysis breaking down specifics about the market.

As we all navigate this journey together, please don’t hesitate to reach out to us with any questions or concerns. We’re here to support you.

- First Name Last Name, LIC #License